In February 2007 George Osborne told an audience in Aberdeen that Gordon Brown was squandering the UKs North Sea oil and gas assets for short-term financial gain. Mr Osborne, then shadow chancellor, accused Mr Brown of putting at risk the investment we need, to get the most out of the North Sea.

Four years later Mr Osborne, now the chancellor, stands accused by the industry of repeating the mistakes of his predecessor. His March budget, where he raised the supplementary charge on oil and gas producers profits from 20 to 32 per cent to help pay for a 1p a litre cut in the fuel duty, has been greeted by an industry-wide outcry.

Executives from some of the worlds largest energy companies, including Chevron, Centrica and Total, to smaller explorers such as Valiant Petroleum, have warned the move is likely to have an impact on future investment . With three tax increases in 10 years the UK now offers a less stable investment climate than many African countries, assert some executives.

So far the number of planned investments put on hold has been very small. Statoil, Norways oil and gas major, has postponed $10bn worth of investment in two projects, while Centrica, the owner of British Gas, said last week it might not restart production at its South Morecambe Bay field after maintenance work is completed in about a month. Valiant Petroleum said in March it had decided not to drill a £93m exploration well.

Others say they are reviewing plans for new developments as well as their exploration targets but concede it is still too early to say whether the tax increase will really stop future investment in its tracks. With oil prices still trading above $110 a barrel on Friday despite the recent rout, companies have been reporting big increases in profits and are sitting on robust balance sheets.

Before the tax rise the North Sea had been enjoying something of a renaissance. Although the majors such as BP, Royal Dutch Shell and ExxonMobil had been shedding mature assets in the UK and investing in countries such as Brazil and Russia, activity has been high.

Producers push decouple line

When Centrica, the UK utility, signed a gas supply contract with Qatar in February, the company managed to secure a key concession; unusually, the Gulf state agreed to decouple the price of its gas from the price of oil, writes David Blair, Energy Correspondent.

Whether these two commodities are priced separately or jointly is central to the argument over the UK governments decision to increase the tax on North Sea output.

At present, oil and gas production in UK waters is taxed on the same basis. When the price of a barrel of Brent crude rises above $75, the Treasury imposes the same supplementary tax on the profits made by every barrel of oil equivalent produced, regardless of whether it happens to be oil or gas.

Energy companies want the Treasury to tax oil and gas separately because their prices have de-linked. The two commodities UK prices have diverged significantly: Fridays Brent crude price was $105.15 a barrel. Natural gas sold at 52.95p a therm, equivalent to about half the level of oil.

Both sides are wary of the complexity of taxing oil and gas separately. Malcolm Webb, chief executive of Oil & Gas UK, an industry lobby group, said it should be possible to achieve this without a separate taxation regime.

But Justine Greening, economic secretary to the Treasury, said that gas may sell for a lower price than oil but its cost of extraction is also cheaper. Consequently, the two commodities have comparable profit margins, making it logical for them to be taxed equally.

At the moment, she added, we dont see a need for decoupling.

Last year saw a development surge with $13.8bn of projects approved by the UK government. Discoveries such as the Catcher field last year, an estimated 100m barrel field of the kind long thought to have been depleted, have revived interest among independents and foreign groups such as Korea National Oil Corporation. The companies involved in that project are not household names. Apart from the FTSE 250 Premier Oil, there is Encore, Wintershall, Nautical Petroleum and Agora Oil, all Aim-traded companies that have proliferated in the area in recent years, snapping up assets unwanted by bigger companies.

Despite the outcries of pain from the industry the government has so far refused to budge. The Treasury calculates that rising oil prices have made North Sea producers 50 per cent more profitable during the past two years, justifying the tax increase as a means of capturing some of that value for the public.

Chris Huhne, energy secretary, told the Commons energy select committee on Wednesday that the tax increase would have no significant effect on investment and was justified by the need to repair the national finances.

If people are going to follow their own self-interest which is a fair assumption for this industry as it is for people in the rest of the economy there is not going to be a significant impact on investment from these changes at these oil prices, said Mr Huhne.

Justine Greening, economic secretary to the Treasury, told the same committee that, given the high oil price, very few new projects would become uneconomic as a result of this tax change.

The dominant factor driving investment is around oil prices, in other words, the inherent value of whats there in the North Sea basin, she said.

Industry executives counter that even if the oil price has boosted profits, the tax rise makes the UK, already a mature area, less competitive on a global scale.

Their argument focuses on the fact that marginal fields have become more uneconomic on the back of the tax increase and that the tax makes no distinction between oil and gas even though the gas price is trading below that of oil.

The government needs to recognise that every field is different, says Peter Buchanan, chief executive of Valiant, adding that we have to guard against a blunt instrument with unintended consequences.

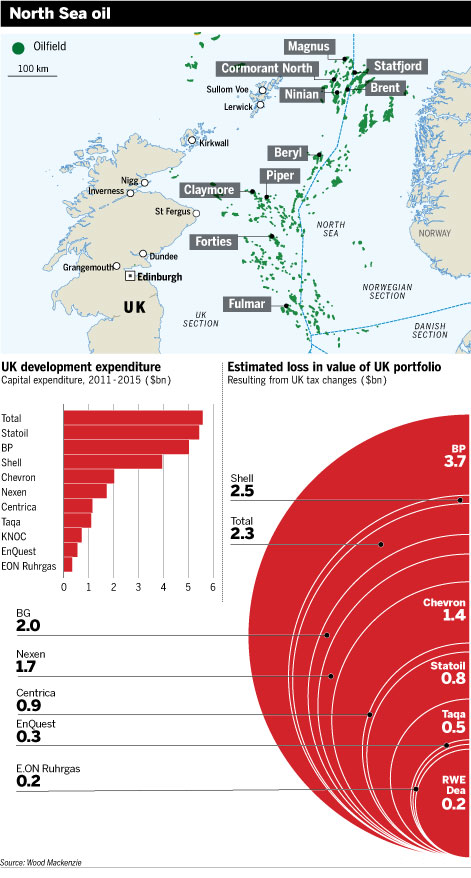

An analysis by Wood Mackenzie, the consultancy, reveals the tax change has reduced the value of companies UK exploration and production portfolios by an average of 21 per cent.

The relative effect on the majors reflects the scale of their UK operations. BP, for example, has seen the value of its portfolio drop $3.67bn, although the fall is relatively small in a global context, accounting for 2 per cent of its global upstream value. By comparison, EnQuest, the North Sea-focused oil explorer, has seen the value of its UK portfolio drop $0.26bn but this represents 19.5 per cent of its total portfolio.

Among the large caps, Nexen saw its portfolio drop $1.7bn, equivalent to 8 per cent of the companys global upstream value.

Geoff Gillies, lead analyst for northwest, central and eastern Europe at Wood Mackenzie, said: At current high oil prices, few new projects will become uneconomic as a result of the change. However, the uncertainty created will impact investment decisions, in particular reinforcing the perception of fiscal instability. Companies will reassess future projects against other opportunities in their portfolios and there is a risk that some may now rank below other projects and could be delayed or cancelled.

There is some scope for compromise with the possibility the government could introduce a new category of field that qualifies for tax allowances. Such new allowances were introduced in the 2009 Budget to encourage exploitation of, among other things, small fields.

Ms Greening on Wednesday said there will be some fields at the margins that will become uneconomic and thats why we raised in the Budget that we would work with the companies to mitigate the impact.

Perhaps more importantly for those companies focused on gas, Ms Greening also opened a possible window for compromise. The Budget set an oil price of $75 per barrel as the threshold for the higher rate of supplementary tax but Ms Greening said the Treasury was prepared to consult on this trigger price.

|