|

|

|

|

|

By STANLEY REEDDEC.

A BP oil platform in the North Sea, about 100 miles east of Aberdeen. Credit Pool photo by Andy Buchanan

LONDON Back in September, when oil was still selling for close to $100 a barrel, North Sea energy reserves were the big prize at stake in Scotlands referendum on whether to secede from Britain.

The Scots voted to keep the kingdom united. But three months later, with oil trading in the $60 range, it is now North Sea oil whose future hangs in the balance.

With a 40 percent fall in prices since June, oil producers around the globe are having to recalibrate. Rosneft is gauging the effects of the price on the Russian economy. OPEC nations are wondering how long they can let market prices threaten their cartel. And Texas shale-oil producers are contemplating whether to start another fracking project.

Perhaps nowhere else in the global oil industry has the question of moving forward been as clouded by doubt as in the North Sea.

Fall in Oil Prices Poses a Problem for Russia, Iraq and Others

A hydraulic fracturing well in Colorado. With the technology, America is expected to surpass Saudi Arabia in oil production.

Free Fall in Oil Price Underscores Shift Away From OPEC

If Brent crude, the North Sea benchmark, remains around $60 to $70, at least 85 percent of new British offshore oil and gas resources now in the planning stages are at risk of being dropped, according to the industry consultants Wood Mackenzie.

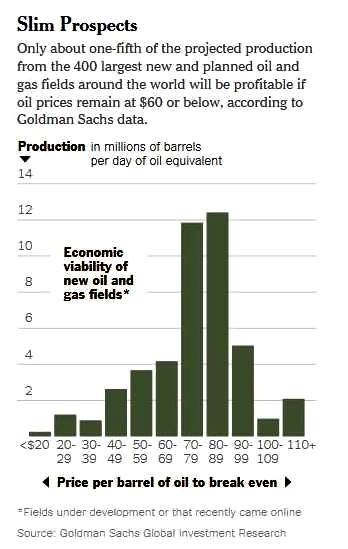

Slim Prospects

Only about one-fifth of the projected production from the 400 largest new and planned oil and gas fields around the world will be profitable if oil prices remain at $60 or below, according to Goldman Sachs data.

That could mean the abandonment of $27 billion worth of planned development and a threat to the jobs of many of the nearly half a million people in Britain who work directly or indirectly in the oil industry. And at current prices, many older North Sea oil and gas fields could begin losing money, potentially causing them to be shut down.

It is very hard to keep some businesses afloat at current oil prices, said Mike Tholen, economics director at Oil & Gas UK, a trade association.

How quickly things have changed.

The past few years had been a boom time for the British oil industry and its thriving hub, Aberdeen, Scotland. With oil prices mostly stable and consistently above $100, companies were investing at record levels, willing to spend whatever was necessary to keep the petroleum flowing and to bring new resources onstream even if it meant venturing farther and deeper offshore.

Even before the price plunge, though, the projected cost of some of the most ambitious North Sea projects was making some companies hesitant. BG, the British oil and gas producer, decided this summer to delay its main North Sea project, Jackdaw, when the projected price tag had risen to $5 billion.

Chevron likewise delayed a flagship development, Rosebank, in hopes of lowering the break-even point, which Goldman estimates to be $87.50 a barrel for it.

Now, with prices for Brent crude far below that level at $60.44 on Friday the economics of finding and developing those deepwater fields look more daunting. The British oil giant BP, a North Sea leader, recently sent letters to recruitment agencies in Aberdeen, saying it would have to cut wages up to 15 percent for any new oil-worker contractors.

The industrys deteriorating economics threaten to accelerate the long-term decline of production in the British North Sea, now about 1.4 million barrels per day of oil and gas, as new projects are delayed and exploration budgets are cut.

Continue reading the main story Continue reading the main story

Continue reading the main story

Similar forces are playing out in other parts of the world.

A big cause of oils falling price, besides a slow economy in many parts of the world, is the previously high price. Years of $100 or more for a barrel of oil encouraged the development of oil from shale rock deposits in the United States, as well as other new sources elsewhere, resulting in big increases in the global supply.

A recent study by Goldman Sachs estimates that many large new oil and gas projects being planned around the world will not be commercially viable with oil at $70 per barrel.

The shale revolution is making $1 trillion worth of new oil projects potentially obsolete, said Michele della Vigna, a London-based Goldman analyst. The industry needs to reduce costs by 30 percent to go ahead with these projects at the current oil price.

If prices stabilize and then bounce back quickly, then the recent drop might soon be forgotten. But a sizable group of analysts say that rather than experiencing a passing blip, the market is undergoing a lasting adjustment to greater abundance of oil and muted economic demand.

In Britain especially, executives concede that production costs were allowed to run out of control. Overall operating costs in British waters increased by 15.5 percent, to 9 billion pounds, or about $14 billion, in 2013, according to Oil & Gas UK. The cost of producing a barrel of oil or gas has been rising at about 20 percent per year, to £17 per barrel.

Costs per field vary greatly. But 19 North Sea oil fields about 6 percent of the total now have costs of more than £30 per barrel, which puts them in danger of losing money.

No wonder companies are scrambling to cut costs. Conoco Phillips, the large American company, said recently that it would reduce its work force in Britain by about 230 people, to about 1,400.

Wood Group, a global oil services company based in Aberdeen, said on Wednesday that it would cut the pay rates for its 1,250 North Sea contract workers by up to 10 percent and freeze the salaries of 4,000 Britain-based employees. These measures have not been taken lightly, but we believe they are required, Dave Stewart, the companys managing director for Britain, said in a statement.

Mr. Tholen of Oil & Gas UK said the fields in the most difficulty were in the northern part of the North Sea. These units, he said, tend to have old pipelines and platforms, which are costly to maintain, while declining production means there are fewer barrels and lower revenue to pay for the operating costs.

If we have a sustained period in which prices remain in the 50s, he said, you can expect to see parts of infrastructure in the North Sea disappearing.

The main deterrent to shutting down fields may be the high costs of closing wells and safely disposing of platforms and other offshore equipment. The industry spent £900 million on such decommissioning last year and is expected to spend nearly £15 billion more through 2023.

For the biggest companies, the best bet now may be to wait out the winnowing. With the billions of dollars in cash reserves, built up during the boom, they can probably afford to let the shakeout run its course even if the North Sea will not necessarily be where they will put as much emphasis when things pick up.

They can figure that the prices of drilling rigs and related equipment like floating production platforms will be cheaper, as demand for the gear ebbs and they are no longer bidding against one another for the services of shipyards in South Korea and elsewhere.

If you have a bit of cash it will go much further in the future, said Malcolm Dickson, an analyst at Wood Mackenzie. Thats one of the silver linings for the oil industry.